Related Articles

Release date: 03/02/2023

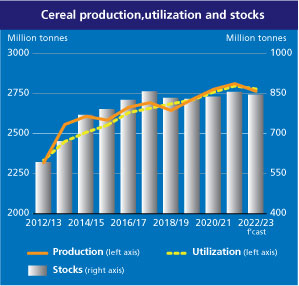

FAO’s latest forecast for world cereal production in 2022 has been raised by 8.3 million tonnes (0.3 percent) this month to 2 765 million tonnes, albeit still 1.7 percent lower year-on-year. The increase is predominantly related to wheat, reflecting upward revisions made for Australia and the Russian Federation, which raised the forecast for the global wheat output to 794 million tonnes and reinforced the expectations for a record-high outturn in 2022. For coarse grains, global production is pegged at 1 459 million tonnes in 2022, moderately down compared to the preceding forecast in December and now 3.3 percent below the level in 2021. The most recent cut reflects lower maize production estimates for the European Union, the United States of America and the Russian Federation, which more than offset an upward revision for China. The forecast for the world barley outturn has been raised moderately, resting on an upturn in harvest prospects in Australia, while the forecast for global sorghum production remains unchanged from December.

As for rice, assessments released by Chinese officials in December, point to a lower level of plantings than previously envisaged by FAO, especially in north-eastern producing areas, which added to some yield decreases caused by heat and dryness in the southern parts of the country. The downward revision for rice production in China more than offset upward revisions made for several other countries, most notably Bangladesh, where authorities report positive outcomes for the second most important crop of the season, despite some rainfall-related setbacks at the planting stage. As a result, global rice production is now forecast in the order of 512 million tonnes (milled basis), down 1.2 million tonnes lower than the December forecast and 2.6 percent from the 2021 all-time high.

Looking ahead to production in 2023, the bulk of the winter wheat crop has been planted in the northern hemisphere and early indications point to area expansions in several major producing countries, driven primarily by the elevated prices. While fertilizer prices dropped in recent months, they continue to be high, which could result in reduced application rates with likely adverse implications for yields. In the United States of America, 2023 winter wheat planted area is estimated to be the largest area in eight years, up 11 percent year-on-year. Drought conditions are affecting the main producing Central Plains and are forecast to continue in the next months; however, the dry weather has partly receded elsewhere, leading to improvements in crop conditions.

In Canada, while the bulk of the wheat crop is planted in spring, and although a pullback in winter sowings is foreseen, total wheat plantings are predicted to expand by 2 percent in 2023, underpinned by remunerative crop prices. In the European Union, official winter wheat area estimates are not yet available, but aided by generally conducive weather and supported by prevailing price incentives, sowings are anticipated to remain above the previous three-year average and close to the 2022 level. In the United Kingdom of Great Britain and Northern Ireland, expectations indicate a 1 percent upturn in winter wheat sowings, supported by beneficial weather and robust output prices.

In the Russian Federation, ample domestic availabilities and low domestic prices could result in a small cutback in wheat plantings. In Ukraine, severe financial constraints, infrastructure damage and obstructed access to fields in parts of the country have resulted in an estimated 40 percent year-on-year reduction in the 2023 winter wheat area. In India, spurred by higher market and government-guaranteed prices, as well as beneficial sowing conditions, the 2023 wheat acreage is anticipated to exceed last year’s record level. In Pakistan, 2023 wheat sowings are foreseen to remain higher than the five-year average, with standing water from the large-scale floods in 2022 causing less hindrance than initially anticipated.